skimmer known as Baka[1], cybersecurity

researchers have uncovered a new flaw in the company’s EMV enabled

cards that enable cybercriminals to obtain funds and defraud

cardholders as well as merchants illicitly.

The research[2], published by a group of

academics from the ETH Zurich, is a PIN bypass attack[3]

that allows the adversaries to leverage a victim’s stolen or lost

credit card for making high-value purchases without knowledge of

the card’s PIN, and even trick a point of sale (PoS) terminal into

accepting an unauthentic offline card transaction.

All modern contactless cards that make use of the Visa protocol,

including Visa Credit, Visa Debit, Visa Electron, and V Pay cards,

are affected by the security flaw, but the researchers posited it

could apply to EMV protocols implemented by Discover and UnionPay

as well. The loophole, however, doesn’t impact Mastercard, American

Express, and JCB.

Security and

Privacy[4] to be held in San

Francisco next May.

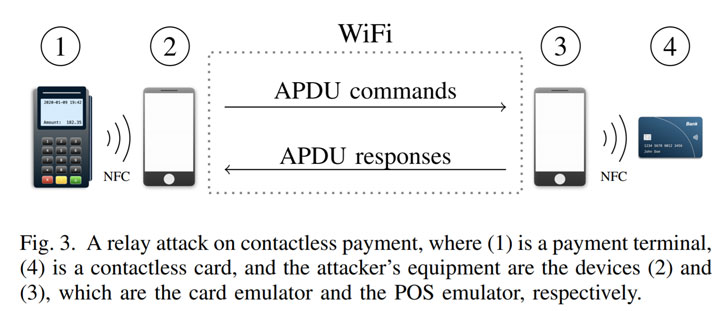

Modifying Card Transaction Qualifiers Via MitM Attack

EMV[5]

(short for Europay, Mastercard, and Visa), the widely used

international protocol standard for smartcard payment, necessitates

that larger amounts can only be debited from credit cards with a

PIN code.

in the protocol to mount a man-in-the-middle (MitM) attack via an

Android app that “instructs the terminal that PIN verification is

not required because the cardholder verification was performed on

the consumer’s device.”

The issue stems from the fact the Cardholder verification method

(CVM), which is used to verify whether an individual attempting a

transaction with a credit or debit card is the legitimate

cardholder, is not cryptographically protected from

modification.

As a result, the Card Transaction Qualifiers (CTQ) used to

determine what CVM check, if any, is required for the transaction

can be modified to inform the PoS terminal to override the PIN

verification and that the verification was carried out using the

cardholder’s device such as a smartwatch or smartphone (called

Consumer Device Cardholder Verification Method or CDCVM).

Exploiting Offline Transactions Without Being Charged

Furthermore, the researchers uncovered a second vulnerability,

which involves offline contactless transactions carried out by

either a Visa or an old Mastercard card, allowing the attacker to

alter a specific piece of data called “Application Cryptogram” (AC)

before it is delivered to the terminal.

Offline cards are typically used to directly pay for goods and

services from a cardholder’s bank account without requiring a PIN

number. But since these transactions are not connected to an online

system, there is a delay of 24 to 72 hours before the bank confirms

the transaction’s legitimacy using the cryptogram, and the amount

of the purchase is debited from the account.

A criminal can leverage this delayed processing mechanism to use

their card to complete a low-value and offline transaction without

being charged, in addition to making away with purchases by the

time the issuing bank declines the transaction due to the wrong

cryptogram.

“This constitutes a ‘free lunch’ attack in that the criminal can

purchase low-value goods or services without actually being charged

at all,” the researchers said, adding the low-value nature of these

transactions is unlikely to be an “attractive business model for

criminals.”

Mitigating PIN bypass and offline attacks

Aside from notifying Visa of the flaws, the researchers have also

proposed three software fixes to the protocol to prevent PIN bypass

and offline attacks, including using Dynamic Data Authentication

(DDA) to secure high-value online transactions and requiring the

use of online

cryptogram[6] in all PoS terminals,

which causes offline transactions to be processed online.

“Our attack show[ed] that the PIN is useless for Visa

contactless transactions [and] revealed surprising differences

between the security of the contactless payment protocols of

Mastercard and Visa, showing that Mastercard is more secure than

Visa,” the researchers concluded. “These flaws violate fundamental

security properties such as authentication and other guarantees

about accepted transactions.”

References

- ^

Baka

(usa.visa.com) - ^

research

(emvrace.github.io) - ^

PIN bypass attack

(arxiv.org) - ^

Security and Privacy

(www.ieee-security.org) - ^

EMV

(en.wikipedia.org) - ^

use of online cryptogram

(www.emvco.com)

Read more http://feedproxy.google.com/~r/TheHackersNews/~3/2FDGcEtP3Yg/emv-payment-card-pin-hacking.html